| (803) 791-1111 | CLIENT LOG IN

Blog Layout

Keys to prevailing through stock market declines

Feb 17, 2020

Download this Article

During periods of volatility in the stock market you may have doubts about your long-term investment strategy. Here are five tips to help you avoid common pitfalls and stay on track toward achieving your financial goals.

1. Declines have been common and temporary occurrences.

Problem:Declines can cause imprudent behavior by filling investors with dread and panic.Solution: Realize that declines are inevitable and have not lasted forever.History has shown that stock market declines are a natural part of investing. While declines have varied in intensity and frequency, they have been somewhat regular events.It may also reassure you to know that the market has always recovered from declines. Although past results don’t guarantee future results, remembering that downturns have been temporary may help assuage your fears.The bottom line? Accept declines as a normal part of the investment cycle.

2. Proper perspective can help you remain calm.

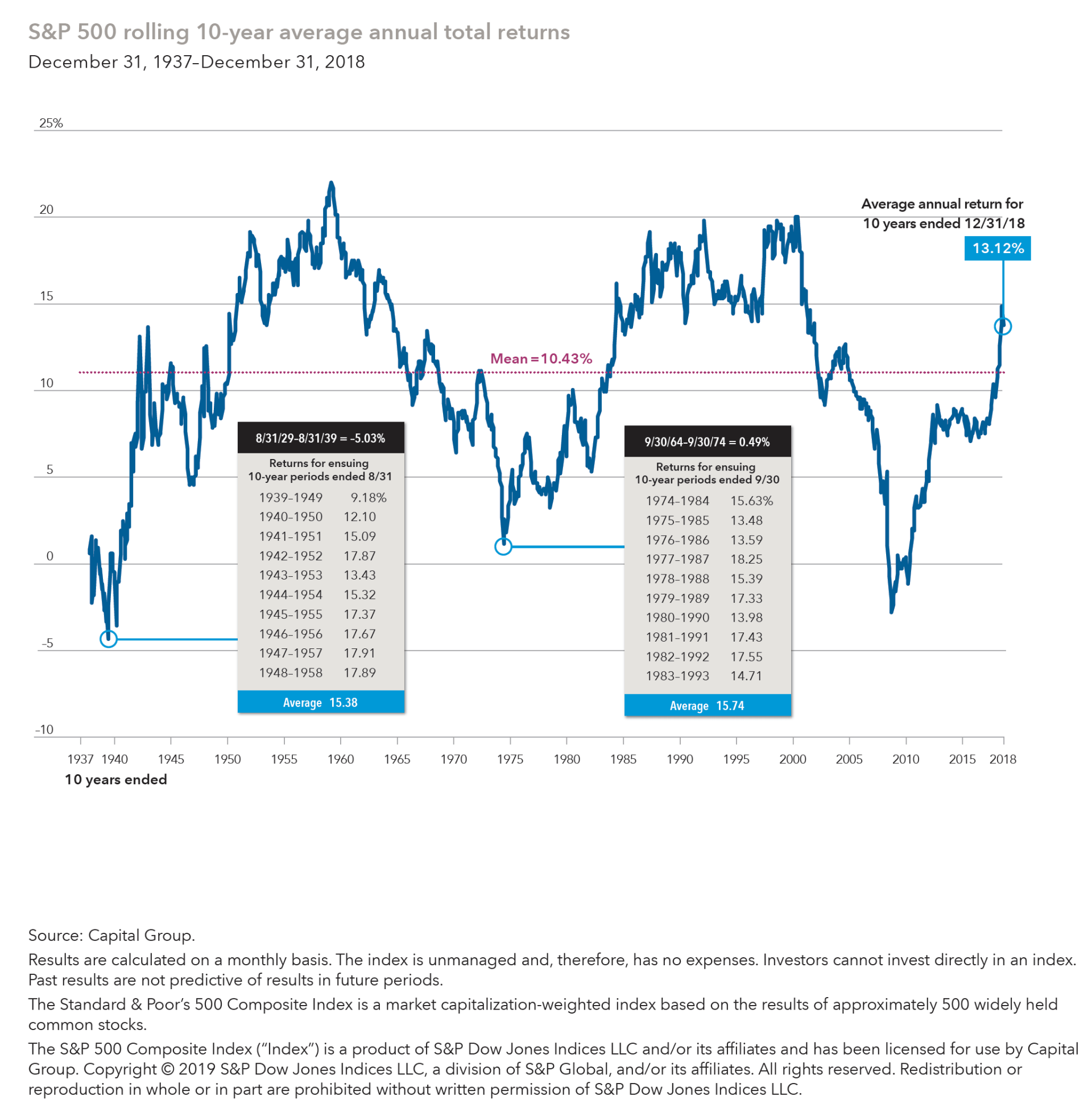

Problem: Studies show that people place too much emphasis on recent events and disregard long-term realities.Solution: Even amid a market downturn, remember that stocks have rewarded investors over time.The stock market has a reassuring history of recoveries. After hitting lows in August 1939 and September 1974, the Standard & Poor’s 500 Composite Index bounced back strong, averaging annual total returns of more than 15% over the next 10 rolling 10-year periods in both cases.Long-term investors have been rewarded.Even including downturns, the S&P 500’s mean return over all rolling 10-year periods from 1937 to 2017 was 10.43%.The bottom line? A long-term perspective can help you prevail through challenging times.

3. Proper perspective can help you remain calm.

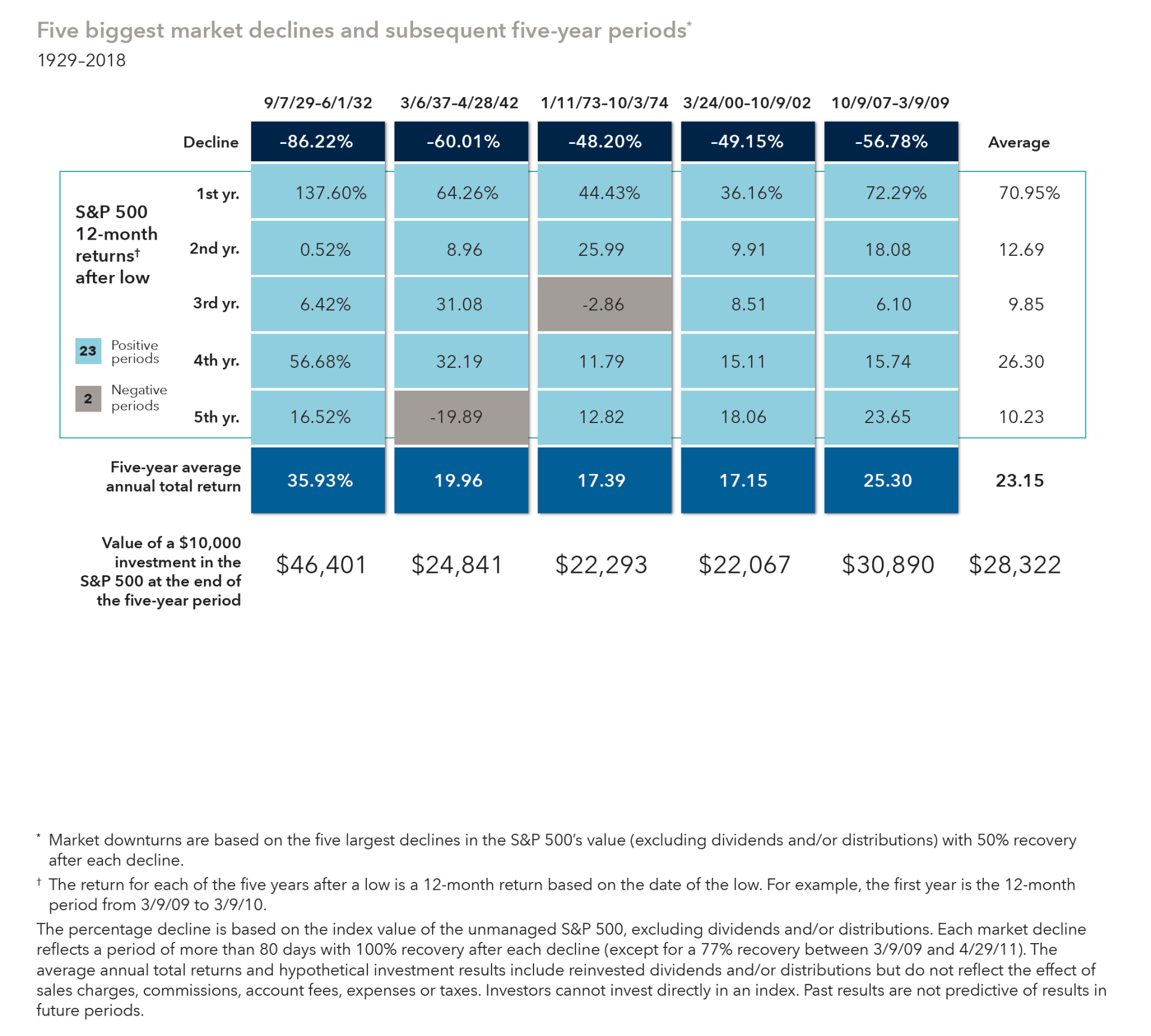

Problem: Research has shown that losses feel twice as bad as gains feel good.Solution: Keep in mind that fleeing the market to reduce losses could mean losing out on gains when stocks recover.The market has shown resilience. Every S&P 500 downturn of about 15% or more since the 1930s has been followed by a recovery.Recoveries have been strong. Returns in the first year after the five biggest market declines since 1929 ranged from 36.16% to 137.60%, and averaged 70.95%. Over a longer term, the average value of an investment more than doubled over the five years after each market low.Don’t miss out on potential market rebounds. Although recoveries aren’t guaranteed, taking your money out of the market during declines means that if you don’t get back in at the right time, you’ll miss the full benefit of market recoveries.The bottom line? Consider staying invested — and don’t try to time the market.

4. Capital Group, home of American Funds, has helped investors prevail through market declines.

Problem: Market indexes don’t tell the whole story and can needlessly alarm investors.Solution: Consider investing in funds run by investment managers who have proven long-term track records.Certain skilled investment managers have superior long-term track records.American Funds is among those proven managers with a long history of success, stemming from our long-term perspective and our emphasis on producing results that are less volatile than the broad market. Equity funds have beaten their Lipper peer indexes in 92% of 10-year periods and 99% of 20-year periods.* Fixed income funds have helped investors achieve diversification through attention to correlation between bonds and equities.† These periods include good times and bad.The bottom line? Invest for the long term with an investment manager that has a proven track record of success — in downturns as well as in bull markets.

5. Emotions can cloud your judgment.

Problem: Investors often make poor decisions when they let their emotions take over.Solution: Stay focused on your long-term goals and carefully consider your options.Have you heard the investment adage, “buy low, sell high”? Strong emotions during market swings can tempt you to do the opposite — buy high and sell low. You may also feel that doing something—anything—during a downturn is better than doing nothing. Although inaction might seem counterintuitive, staying invested in the market could be the better choice.The bottom line? Avoid making rash decisions based on emotions.

Information is provided by Longleaf Advisors and written by Capital Group / American Funds, a non-affiliate of Cetera Advisor Network LLC.

Receive News from longleaf

Thanks to the Tax Cuts and Jobs Act of 2017, the vast majority of Americans don’t have to worry about paying estate taxes. This legislation increased the estate tax exemption considerably — the exemption amount is currently $12.06 million per person, or $24.12 million for a married couple filing jointly. This means that for any individual or couple whose estate is worth less than this at the time of their death, no estate tax will be assessed. In recent years, just 0.2% of the estates of Americans who have died have owed estate tax, according to IRS data. Higher Exemptions are Expiring Unfortunately, this could all change drastically in just a few years when the higher gift and estate tax exemptions expire. The exemption amounts are currently scheduled to sunset on December 31, 2025, or in just over three years. When this happens, the gift and estate tax exemption will be cut in half to approximately $6 million per person, or $12 million for a married couple filing jointly. A hypothetical example illustrates the potential impact of this change on an estate. Let’s say that the Smiths, who have an estate worth $30 million, die in 2022. Just under $6 million ($5.88 million to be exact) of their estate will be taxable when you factor in the $24.12 million estate tax exemption. At the highest estate tax rate of 40%, this would result in an estate tax of about $2.35 million. But what if the Smiths live for a few more years and die in 2026 instead of this year? In this case, approximately $18 million of their estate will be taxable. At the highest estate tax rate of 40%, this would result in an estate tax $7.2 million — or nearly $5 million more than if they died before the end of 2025. How to Lower Estate Taxes with an ILIT This upcoming change in estate tax law makes it critical for affluent individuals and families to plan now for ways they can reduce estate taxes in the years ahead. One effective tool for lowering estate taxes is an irrevocable life insurance trust, or an ILIT. The purpose of an ILIT is to reduce the value of your taxable estate by removing life insurance proceeds from your estate, thus shielding them from estate taxes. Proceeds from the policy’s death benefit are deposited into the trust where they’re held on behalf of your beneficiaries. This shields them from taxation. Meanwhile, your beneficiaries will receive the death benefit tax-free upon your death. They can then use this money to pay any estate taxes that may be due (or any other outstanding debts or expenses) without having to sell assets to cover the estate tax bill. The Nuts and Bolts of ILITs There are three parties to an ILIT: the grantor, the trustee and the beneficiaries. The grantor is the person or couple establishing and funding the trust, the trustee is the party managing the trust and the beneficiaries are the recipients of the trust distributions. You can name anyone you want as the trustee, including your spouse, an adult child, a close friend, an attorney or a financial institution. Your trustee may have discretionary authority to control when beneficiaries receive life insurance policy proceeds. For example, proceeds can be paid in full upon your death or when beneficiaries reach a certain age or life milestone such as graduating from college or having a child. As the grantor, you can transfer ownership of an existing life insurance policy to an ILIT after the trust is formed or the trust can purchase the policy directly. When you die, the life insurance policy’s death benefit is deposited into the ILIT and held in trust for your beneficiary or beneficiaries. If your spouse is the beneficiary, he or she will receive regular incremental payments instead of a lump sum that won’t be taxed as part of your spouse’s eventual estate. In addition to potentially reducing estate taxes, an ILIT can also help protect assets from creditors. Any coverage amounts above your state’s creditor limits held in an ILIT are generally protected from the grantor’s or beneficiary’s creditors. The biggest drawback of an ILIT is that, as the name implies, it is irrevocable. This means that no changes can be made once the trust is finalized, nor can you dissolve the trust. Any assets that you as the grantor place in the trust no longer belong to you and you have no control over them. How We Can Help We can help you determine whether an irrevocable life insurance trust might play a helpful role in your estate plan. Give us a call at (803) 791-1111 or send us an email to talk about your situation in more detail. Information is provided by William Amick & Blake Amick and written by Don Sadler, a non-affiliate of Cetera Advisor Networks LLC. This post is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate professional should be sought. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable by having the policy approved. As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications. Investment Advisor Representatives offering securities and advisory services through Cetera Advisor Networks LLC, member FINRA/SIPC, a broker/dealer and Registered Investment Adviser. Cetera is under separate ownership from any other named entity. 171 Lott Ct, West Columbia, SC 29169

Within the context of employee retirement plans, a fiduciary is responsible for ensuring the plan is managed with the best interest of participants in mind. ERISA identifies three different types of employee benefit plan fiduciaries and specifies reporting and disclosure requirements for them. Each of these types of fiduciaries serves a unique role in plan management, administration and support. It’s important to understand these roles so you choose the right type of fiduciary for your plan. 3(16) Advisor: Overseeing Plan Administration and Operations The first type of fiduciary is known as a 3(16) advisor, whose main responsibilities are overseeing plan administration and daily operations. This fiduciary’s tasks typically include the following: •Distributing summary plan descriptions, benefit statements and required disclosures to participants •Maintaining and interpreting the plan document •Ensuring timely deposit of participant contributions •Fulfilling reporting requirements •Soliciting and enrolling new members You can hire an outside third-party administrator (TPA) to handle these responsibilities if you prefer. However, this does not relieve you of your fiduciary duties and liabilities. For example, you still must oversee the TPA’s activities and monitor the fees charged to make sure they are reasonable. Note that TPAs usually will not agree to sign Form 5500 or be named the plan administrator. You will retain this responsibility as the plan sponsor, along with fiduciary liability for administering all other plan duties and monitoring the prudence of the administrator selection. 3(21) Advisor: An Investment Professional The second type of fiduciary is known as a 3(21) advisor who serves as a financial advisor to the plan. This fiduciary role is usually filled by an outside investment professional who charges a fee. 3(21) advisors make recommendations and offer advice about how plan assets are invested, and sometimes help ensure that the plan is complying with ERISA’s investment-related provisions. Importantly, 3(21) advisors do not actually make investment decisions — this responsibility lies with the plan administrator. A 3(21) advisor might present the plan administrator with a list of investment options that meet the plan’s objectives. As a result, the fiduciary responsibility and liability of a 3(21) advisor is limited. 3(38) Advisor: Going a Step Further The third type of fiduciary is known as a 3(38) advisor. This fiduciary goes a step further than a 3(21) advisor by actually making investment decisions and purchasing securities. Banks, insurance companies and Registered Investment Advisors (RIAs) usually serve as 3(38) advisors. A 3(38) advisor has full fiduciary responsibility to manage the retirement plan and make investment decisions that are in the best interests of plan participants while maintaining transparency about these decisions. This includes providing investment performance reports to the plan sponsor. While the 3(38) advisor has the final authority to make investment decisions, the 3(16) fiduciary can replace the 3(38) advisor if performance is deemed unsatisfactory. Choosing the Right Fiduciary As a plan sponsor, it’s critical that you understand the three different types of employee benefit plan fiduciaries and their specific roles so you choose the right one for your particular circumstances. We can answer any questions you have about retirement plan fiduciary support and help you make the right choice for your plan. Give us a call at (803) 791-1111 or send us an email if you’d like to talk about your plan in more detail. Information is provided by William Amick & Blake Amick and written by Don Sadler, a non-affiliate of Cetera Advisor Networks LLC. This post is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate professional should be sought.

Most of us don’t like to think about our own mortality. But as the owner of a closely held business, you have a responsibility to plan for what would happen to your company if you were to unexpectedly die or become disabled. Without a succession plan, the future of your business could be at risk if this were to occur. Failing to create a succession plan could also be financially dangerous for your family and employees who might have to scramble to pick up the pieces in your absence. Here are 6 factors to consider as you think about creating a succession plan for your business. 1. Get started early It’s never too early to start thinking about business succession and creating a plan. If fact, you should have some idea of your eventual business endgame on the day you start your business. It takes time for a business succession plan to evolve and take shape. Therefore, you should start thinking seriously about business succession and creating a plan at least five years before your planned exit from the company. 2. Define roles and identify potential future leaders Give some thought to what your company’s future leaders should look like and the skills and character traits they should possess. For example, do they need technical expertise? What about people and management skills? These are often more important for leaders than technical or product knowledge. Once you have an idea of leadership roles, you can start looking for good potential candidates. They could be current employees or you might need to look for outside talent. Your choice of a successor CEO, of course, will be most critical, so plan to focus most of your attention and efforts on this. 3. Begin preparing future leaders for their roles This will require you to take on more of a mentorship role with employees you’re going to tap as future leaders. In some respects, you may want to “clone” yourself by teaching them everything you’ve learned over the years about managing and growing your business. This will require an investment of time and energy, but it’s critical to help ensure a smooth succession. Also think about what kinds of training and education future leaders will need and make sure they receive this during the transition period. For example, they might need industry technical certifications or advanced degrees (such as an MBA) or training in the areas of organization, leadership and strategy. 4. Identify types of potential buyers Business buyers fall into one of two broad categories: internal or external. Internal buyers are existing employees (especially top managers and executives) or family members (in a family business). Employee stock ownership plans (ESOPs) and management buyouts (MBOs) are commonly used to accomplish these types of purchases. External buyers fall into one of two different categories: financial buyers and strategic buyers. Financial buyers include private equity groups that are looking for businesses with high growth potential that they can sell to realize a return on investment. Strategic buyers seek businesses with complimentary products or services. This includes competitors, who can gain market share and consolidate operations by acquiring your firm. 5. Plan for how you can add value to the business There are things you can do before listing your business for sale to increase its value in the marketplace. You should be focusing on these value drivers during the months and years leading up to the business sale. Having clean and accurate financial statements and current, signed customer contracts is one value driver. Another is building a strong “bench” of seasoned, experienced executives and managers who can help ensure a smooth transition to new ownership. One of the main things buyers want to see is strong growth potential, so be sure to create a growth plan that’s realistic and attainable. 6. Get a professional business valuation Many owners have a “gut feeling” about what their business is worth, but this value often isn’t realistic. The fact is, most owners have an emotional connection to their business, which they’ve built through years of sweat equity. So it’s hard for them to look at their business’ value objectively. This is why obtaining a professional business valuation is so important. Buyers examine businesses from a purely analytical approach, based on what the numbers say. In particular, they will look carefully at the quality and consistency of earnings. Having a quality of earnings study performed by a valuation professional will help you estimate your business’ future cash flow potential, which will assist in determining an accurate business valuation. How We Can Help Given its importance, you should consider engaging a professional to help you with business succession planning. Give us a call at (803) 791-1111 or send us an email to talk about how we can help you create a succession plan for your business. Information is provided by William Amick & Blake Amick and written by Don Sadler, a non-affiliate of Cetera Advisor Networks LLC. This post is designed to provide accurate and authoritative information on the subjects covered. It is not, however, intended to provide specific legal, tax, or other professional advice. For specific professional assistance, the services of an appropriate professional should b e sought.